This blog is part of a two-part series. Here, we break down what changed and why it matters for ACOs. Part 2 will focus on execution priorities, margin protection, and 2027 pathway decisions, including how ACOs should evaluate LEAD versus MSSP as ACO REACH sunsets.

Performance Year 2026 is the final chapter of ACO REACH, and the economics of that chapter were deliberately reshaped to set up what comes next. Financial guardrails are tighter, more revenue is at risk for quality, extreme upside and downside are constrained, and benchmarks are anchored more heavily to your own historical cost experience. Together, these changes compress margins while reducing volatility in the program’s final year.

For you as an ACO leader, that combination leaves less room for error, fewer late-cycle levers, and higher exposure if performance slips. ACO REACH will end on December 31, 2026, immediately ahead of the proposed launch of the Long-term Enhanced ACO Design (LEAD) Model on January 1, 2027. The LEAD Model webinar on January 29 and the March 2026 application window make one thing clear: PY 2026 is not just a closing year, it is the proving year for what CMS intends to scale next.

This means that you are being asked to optimize performance in a tightening model while evaluating a successor whose details remain incomplete. The window for informed decision-making is narrower now than any prior model transition.

Why CMS Tightened the Model in Its Final Year

The PY 2026 updates reflect a recalibration, not a punishment. CMS responded to its own evaluation findings and to mounting fiscal pressure on Medicare.

In its PY 2023 ACO REACH evaluation, CMS reported $1.643 billion in gross savings, a 5.8% gross savings rate. After shared savings payments and performance bonuses, however, net Medicare spending increased across participant types. Savings existed on paper but evaporated when the checks went out.

MedPAC echoed this concern in its 2024 and 2025 reports, arguing that historical rebasing and risk adjustment can, under certain conditions, push benchmarks higher over time. While aspects of MedPAC’s methodology have been contested, the policy signal is unmistakable: CMS is acting to limit mechanisms it believes may inflate spending. Think of it as a treadmill where forward progress risks resetting the baseline higher, prompting CMS to slow the belt rather than accelerate it.

At the same time, the Medicare Trustees’ 2024 report underscored the fiscal reality. The worker-to-beneficiary ratio has fallen from 5.1 in 1960 to just 2.8 in 2024. Fewer workers supporting more beneficiaries leaves little tolerance for spending growth that does not translate into real savings.

CMS’s mandate sharpened to protect federal dollars while preserving transformation incentives. ACO REACH, already positioned as a time-limited model, became the proving ground for tighter guardrails.

How PY 2026 Reshapes Your Financial Reality

Each policy change pulls a specific financial lever, and all of them move at once. Each lever creates a corresponding decision risk for your leadership team. Understanding the mechanics without understanding the consequence is where organizations get caught flat-footed.

1. Your Benchmarks Now Reflect Your Own History, Not the Market’s

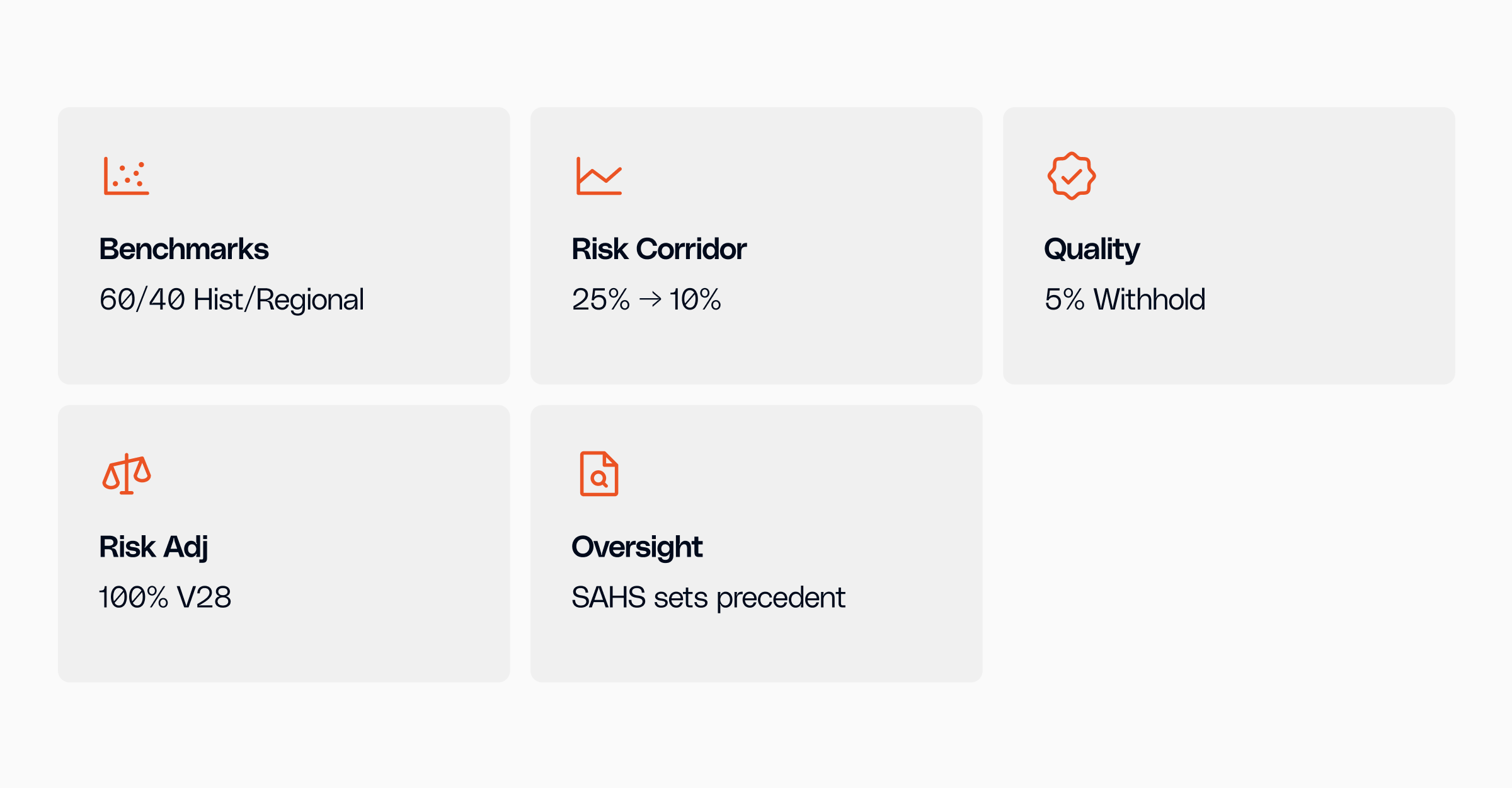

CMS increased the weight of historical expenditures and reduced reliance on regional benchmarks. Standard ACOs now operate under a 60/40 historical-regional blend, up from 55/45. New Entrant and High Needs ACOs shift to 55/45.

Here’s the trap. If you assume regional efficiency will continue to cushion performance, you risk underestimating margin pressure. Historically efficient ACOs face less external uplift, while improvement-focused organizations must recognize that prior gains now tighten future benchmarks. PY 2026 modeling that ignores this shift will overstate achievable savings.

2. Risk Score Growth Hits a Ceiling, but Downside Remains Exposed

CMS introduced a 3% cumulative cap on average risk score growth for Standard ACOs.The retroactive nature means you're being held to a cap for investments made years ago under different methodology, with no ability to course-correct.

This creates real tension for organizations that invested heavily in documentation improvement under prior rules. Under PY 2026 methodology, continuing broad coding expansion without prioritization risks misallocating resources. The danger is in over-investing in an activity that no longer moves the benchmark meaningfully.

3. Extreme Performance Years Matter Less, Consistency Matters More

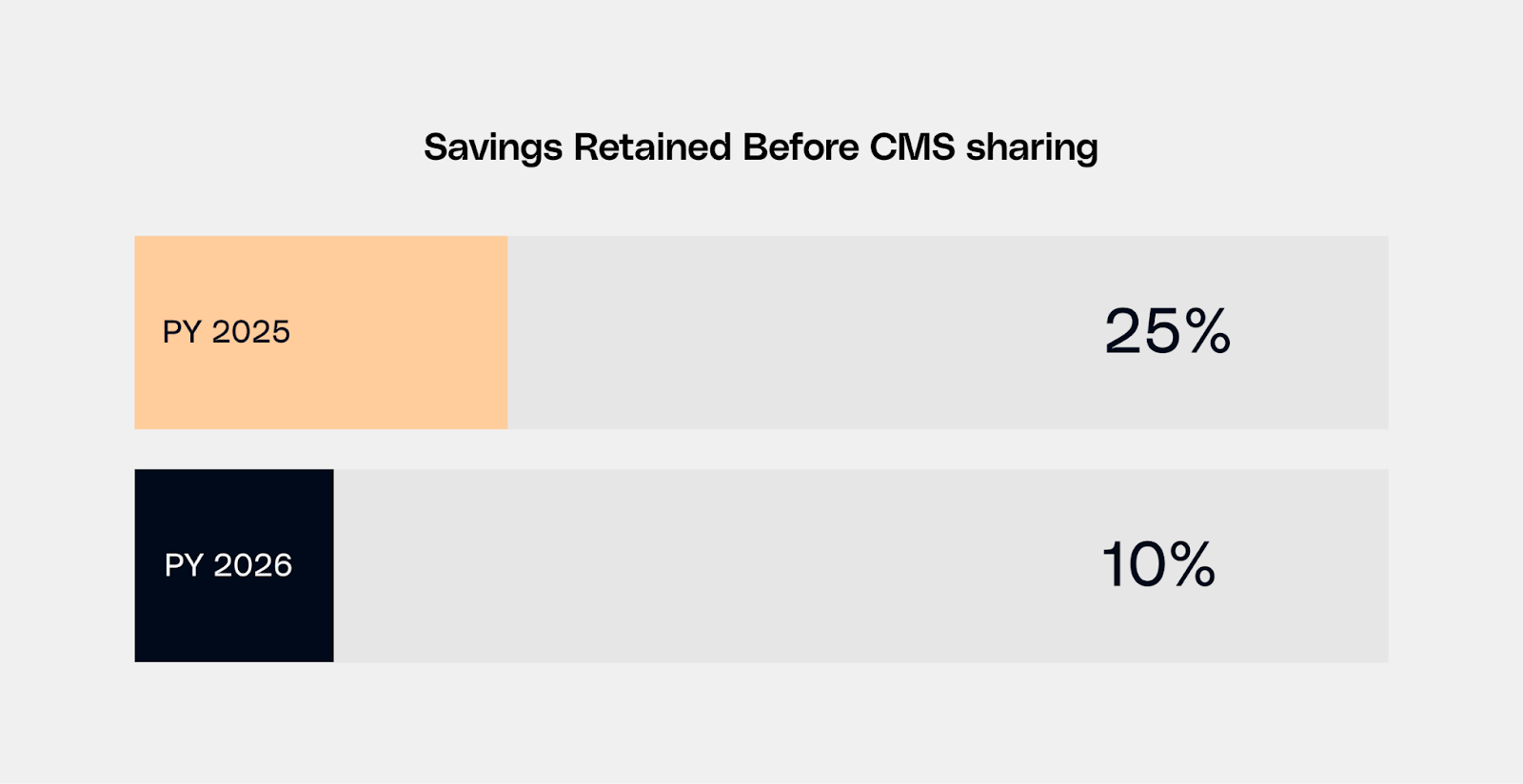

For Global Risk ACOs, CMS narrowed the first risk corridor from 25% to 10%. Savings or losses beyond that threshold are now shared with CMS sooner.

Put simply, an ACO generating 20% savings now retains only 15% instead of the full 20%. If your financial plan relies on breakout years to offset variability elsewhere, that assumption no longer holds. PY 2026 rewards consistency, not volatility.

4. Average Quality Performance Is No Longer Financially Neutral

The quality withhold increased from 2% to 5%, a three-point increase that represents a 150% rise in revenue at risk. CMS data shows the average Total Quality Score in PY 2023 was 78.55%. Only 20 of 77 Standard and New Entrant ACOs (approximately 26%) qualified for the High Performers Pool.

Do the math on your aligned lives. With a 5% withhold, average performance now creates real, irreversible revenue leakage. Quality is now one of the largest drivers of settlement outcomes.

5. V28 Makes Inconsistent Documentation a Source of Financial Volatility

PY 2026 completes the transition to the CMS-HCC V28 risk adjustment model. You move from a 67% V28/33% V24 blend in PY 2025 to 100% V28 in PY 2026. The new model adds new diagnosis categories but makes each category harder to qualify for and worth fewer points.

Combined with the 3% cumulative risk score cap, the V28 transition creates a paradox. You must invest in documentation precision to maintain risk score accuracy, but the cap limits the financial benefit of aggressive coding efforts. Inconsistent documentation practices introduce downside risk without offsetting upside, particularly under capped growth.

The danger is that variability across your provider network erodes predictability. Your aggregate risk score becomes volatile, because your documentation consistency varies.

6. Benchmark Inputs Are No Longer Outside CMS Scrutiny

CMS excluded specific supply-related HCPCS codes from PY 2024 benchmarks due to anomalous national billing patterns. The precedent matters more than the codes themselves.

The agency has shown it will intervene when utilization patterns distort benchmarks. Governance that remains reactive rather than proactive increases exposure to retroactive adjustment.

Why PY 2026 Sets the Tone for What Comes Next

Collectively, these changes compress margin, reduce volatility, and shift risk earlier in the year. That convergence makes PY 2026 fundamentally different from prior performance years.

With rebasing no longer available as a corrective mechanism and benchmarks finalized only after the performance year closes, execution errors in PY 2026 cannot be absorbed or adjusted away.

On December 18, 2025, CMS announced the Long-term Enhanced ACO Design (LEAD) Model, launching January 1, 2027. While the 10-year timeframe is promising, critical details await the March 2026 RFA.

NAACOS President, Emily Brower shared in a statement, “While these components will be beneficial to participants in the long run, launching the model in 2027 does not provide ACO REACH participants with enough time to evaluate alternative payment model options and effectively plan their transition.”

You must simultaneously optimize PY 2026 performance, evaluate LEAD readiness, and model MSSP alternatives all within nine months. Your PY 2026 results will shape your credibility for whatever comes next.

If you need support quantifying how these changes affect your benchmark, quality exposure, or risk profile ahead of the LEAD model RFA, schedule a call with our healthcare actuarial experts.

Stay tuned for Part 2 where we examine how leading ACOs are responding, including execution priorities, margin protection by ACO type, and how to prepare for what comes after ACO REACH without overcommitting too early.